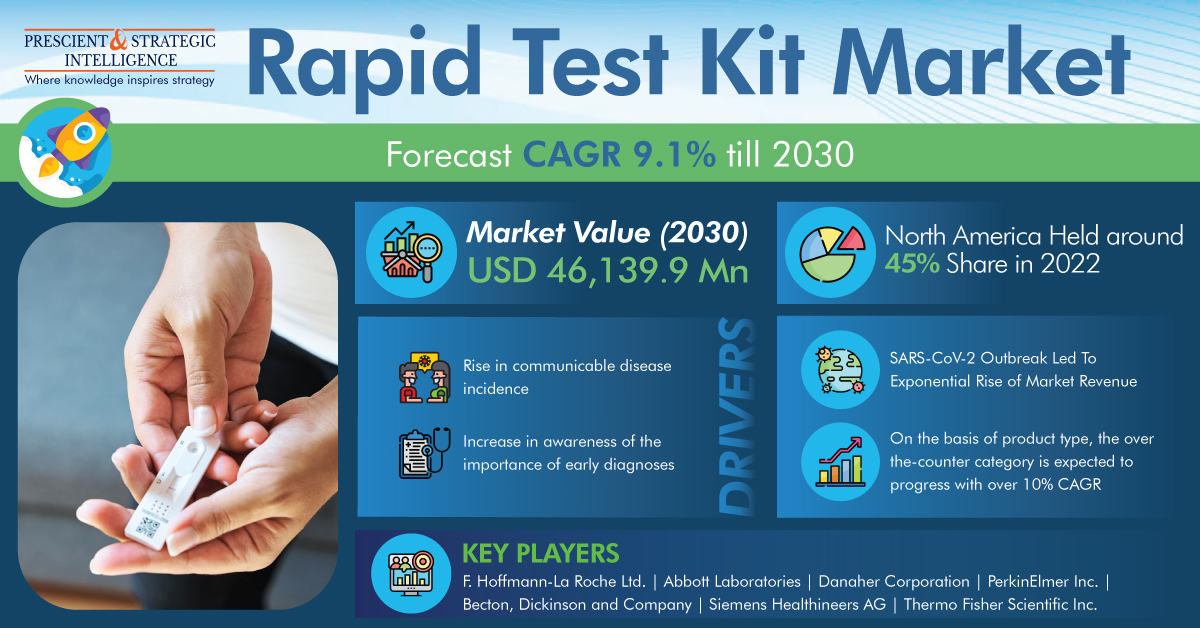

In 2022, the rapid test kit market was worth around USD 23,043.3 million, and it is projected to advance at a 9.1% CAGR from 2022 to 2030, hitting USD 46,139.9 million in 2030, according to P&S Intelligence.

Rapid tests are utilized for initial screening, and for the initial analysis of illnesses. Because of their dependability and quick results, they have extensive applications.

Furthermore, credited to their lucrative and easy-use nature, the diagnoses can be completed with ease of one’s home, which is another factor they are gaining more and more traction in the industry. The increasing infectious disease occurrence, surge in the importance of knowledge of early diagnoses, and growing elderly populace positively impacted the demand for such tests.

The outburst of the novel coronavirus resulted in the sudden and massive development of the industry, because of the growth in the need for quick diagnostic solutions, to eventually stop the serious, life-intimidating difficulties of the virus.

The terror of infectious infection results in individuals accepting such quick point-of-care diagnostic kits to identify the virus early stage, from the ease of their houses. The orders for the accessibility of such kits by governments at several public and private hospitals also boosted the growth of the market.

The increasing frequency of foodborne illnesses leads to a surge in the utilization of rapid diagnostic kits to classify the existence of contaminants, through the testing of a food sample, to avoid difficulties.

Benefits like, specificity, high sensitivity, fast results the capability to spot viruses existing to a low extent, and the removal of the restrictions of orthodox testing approaches make enhanced rapid tests more popular, thus fuelling the market growth. Furthermore, such diagnostic tests are enabled to remove human mistakes, save time and reduce labor.

In 2022, the hospitals and clinics category held the largest rapid test kit market share, of around 50%, on the basis of end users. This can be credited to the surging occurrence of the novel coronavirus infection caused a high hospitalization rate. This multitudes the number of partnerships between the main industry players and several steps by governments worldwide to guarantee the accessibility of test kits for the initial diagnosis of COVID-19, to avoid further damages.

North America had the largest market share, of approximately 45%, in 2022. This can be credited to the existence of deep-rooted medicinal companies in the continent, strong healthcare infrastructure, and high knowledge among the people regarding maintaining well-being.

Hence, with the help of these kits, the diagnoses can be completed with ease of one’s home and also the increasing infectious disease occurrence, the surge in the importance of knowledge of early diagnoses, and the growing elderly populace are major factors driving the rapid test kit market.