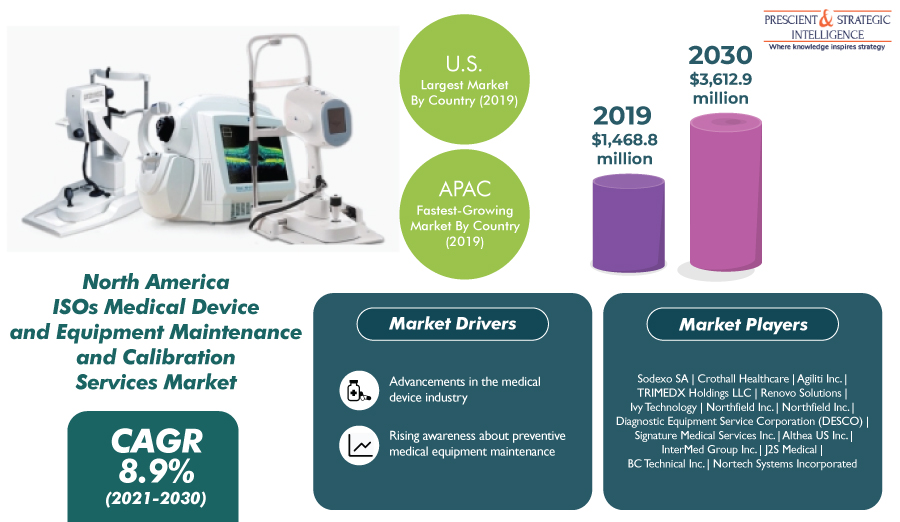

The North America ISOs medical device and equipment maintenance and calibration services market will grow at a rate of 8.9% in the years to come, to reach USD 3,612.9 million by 2030, as stated by a market research institution, P&S Intelligence.

The key factors responsible for the industry growth are progressions in the medical device sector, increase in consciousness regarding preventive medical equipment maintenance, and strict regulatory environment.

The patient monitoring and electromedical category will grow the fastest in the years to come. This has a lot to do with the high incidence of chronic ailments, such as cardiac and respiratory, increasing aging population, and growing number of ICU beds.

The U.S. had a larger share in the North America ISOs medical device and equipment maintenance and calibration services market, and the nation will continue the same way in the years to come. This is mostly because of the occurrence of a large count of hospitals and established players and rise in tech progressions with regards to diagnostic tests.

Medical devices can be employed in numerous applications, not being precise to just one area.

Furthermore, these services also aid in averting infections brought about by the usage of medical devices throughout surgeries.

Therefore, the importance on cleanliness in healthcare institutions is increasing, with a number of prestigious administrations delivering guidance for improving cleanliness and averting infections.

For example, the WHO has given guidelines for hospital hygiene, emphasizing equipment maintenance for infection control.

The incidence of a strict regulatory framework makes medical paraphernalia maintenance a required prerequisite for end users in North America.

For instance, the U.S. CMS regulations and other accreditation necessities TJC, HFAP, and DNV, along with guidelines by OEMs and the USFDA, necessitate compliance with regards to equipment maintenance amongst hospitals.

It is because of the advancements in medical industry, the demand for medical device and equipment maintenance and calibration services in North America will be on the rise in the years to come.