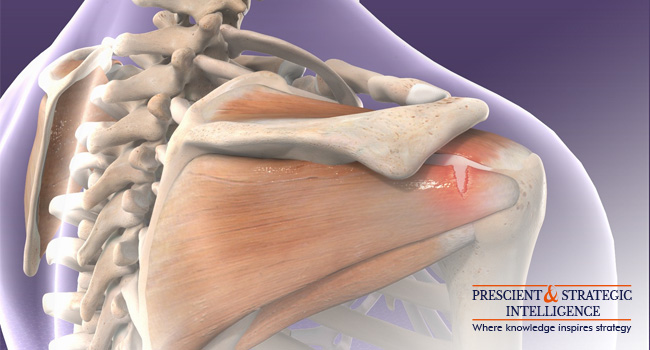

In 2022, the rotator cuff injury treatment market was worth around USD 1,098.4 million, and it is projected to advance at a 5.1% CAGR from 2022 to 2030, hitting USD 1,633.5 million in 2030, as per P&S Intelligence.

This growth can be credited to the increasing frequency of shoulder injuries because of sports, technological advancements in arthroscopic surgery equipment, and snowballing osteoarthritis issues in the elderly populace.

In 2022, The surgical treatment category held the biggest revenue share, approximately 55%, and is projected to continue with the dominant till the end of the decade. Credited to the growing occurrence of rotator cuff injuries and the supportive therapeutic reimbursement for the surgery.

In 2022, North America led the industry by generating the largest revenue share, of approximately 45%. This can be credited to the increasing number of product launches, constant research and development, and commercialization of advanced treatments for rotator cuff injuries.

Furthermore, the snowballing subsidy and a number of partnerships between main businesses, a supportive regulatory environment for rotator cuff operations, along with favorable government guidelines for the sale of related goods fuels the industry. Furthermore, the considerable engagement in sports will enable the continent to continue with its dominance throughout the decade.

Hence, the increasing frequency of shoulder injuries because of sports, technological advancements in arthroscopic surgery equipment, and snowballing osteoarthritis issues in the elderly populace are the major factors contributing in the growth of the rotator cuff injury treatment market.