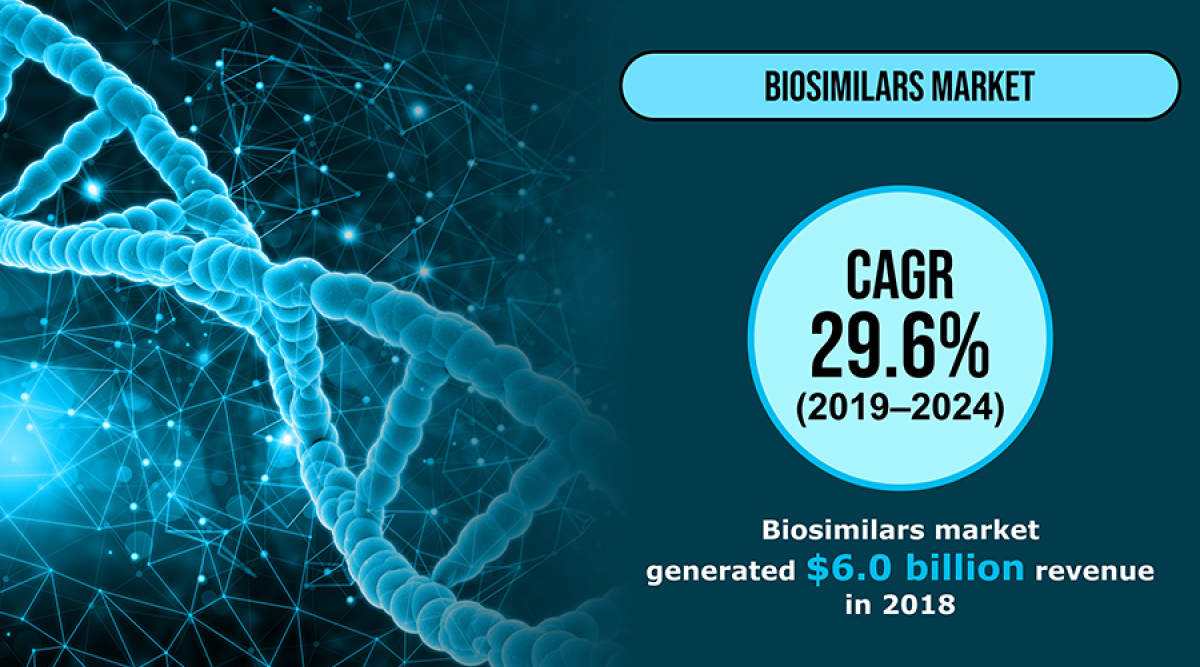

A number of factors such as the increasing incidence of chronic diseases, rising investments in research and development (R&D) initiatives by biopharmaceutical companies, and growing geriatric population will drive the biosimilars market at a robust CAGR, of 29.6%, during the forecast period (2019–2024). Moreover, lower price of biosimilars than reference drugs and presence of an extensive pipeline of these biological products will also catalyze the market growth. The market revenue stood at $6.0 billion in 2018 and it is projected to reach $26.7 billion by 2024.

One of the prime factors contributing to the market growth is the surging incidence of chronic diseases, such as cardiovascular diseases (CVDs) and cancer. According to the World Health Organization (WHO), 2.26 million, 2.21 million, 1.93 million, 1.41 million, 1.20 million, and 1.09 million new cases of breast cancer, lung cancer, colon and rectum cancer, prostate cancer, skin (non-melanoma) cancer, and stomach cancer, respectively, will be recorded across the world in 2020. The WHO also estimates that approximately 17.9 million global deaths occur due to CVDs annually.

At present, companies operating in the biosimilars market are engaging in product launches to march ahead in the competition. For instance, in 2018, adalimumab was launched in the European market by Samsung Bioepis, Sandoz International GmbH, Mylan N.V., and Amgen Inc. These companies aim to launch this product in the U.S. market by 2023. Additionally, the market players are also focusing on partnerships and collaborations to consolidate their position. For example, in June 2018, Biocon India Private Limited collaborated with Sandoz International GmbH to develop, manufacture, and market next-generation biosimilars, such as Etanercept.

The product segment of the biosimilars market is classified into recombinant glycosylated proteins, recombinant non-glycosylated proteins, and recombinant peptides. Under this segment, the recombinant glycosylated proteins category generated the highest revenue in 2018, due to the less complexity, high stability, and smooth approval process of such biosimilars. This category is further classified into follitropin, monoclonal antibodies (mAbs), and erythropoietin (EPO). Among these, the mAbs category is expected to hold the largest market share in coming years, due to the surging usage of such biosimilars in treating cancer and diabetes.

Furthermore, the categories under the indication segment of the biosimilars market include rheumatology, oncology, infectious diseases, chronic diseases, auto-immune diseases, blood-related disorders, growth hormone deficiency (GHD), and others. Under this segment, the oncology category accounted for the largest market share in 2018, owing to the soaring cases of cancer worldwide. As per the WHO, cancer will cause approximately 10 million global deaths in 2020. The organization further estimates that lung cancer, colon and rectum cancer, and liver cancer will be the leading causes of death worldwide, accounting for 1.80 million, 935,000, and 830,000 deaths, respectively, in 2020.

According to P&S Intelligence, the European biosimilars market generated the highest revenue in 2018, due to the burgeoning aging population and mounting investments being made by the biopharmaceutical companies in R&D activities. For instance, the WHO forecasts that the number of individuals aged 85 years and over in Europe will rise from 19 million in 2020 to 40 million by 2050. Besides, the presence of a flexible regulatory framework will also fuel the demand for biosimilars in the region.

Therefore, the soaring cases of cancer and CVDs will facilitate the demand for biosimilars in the forthcoming years.