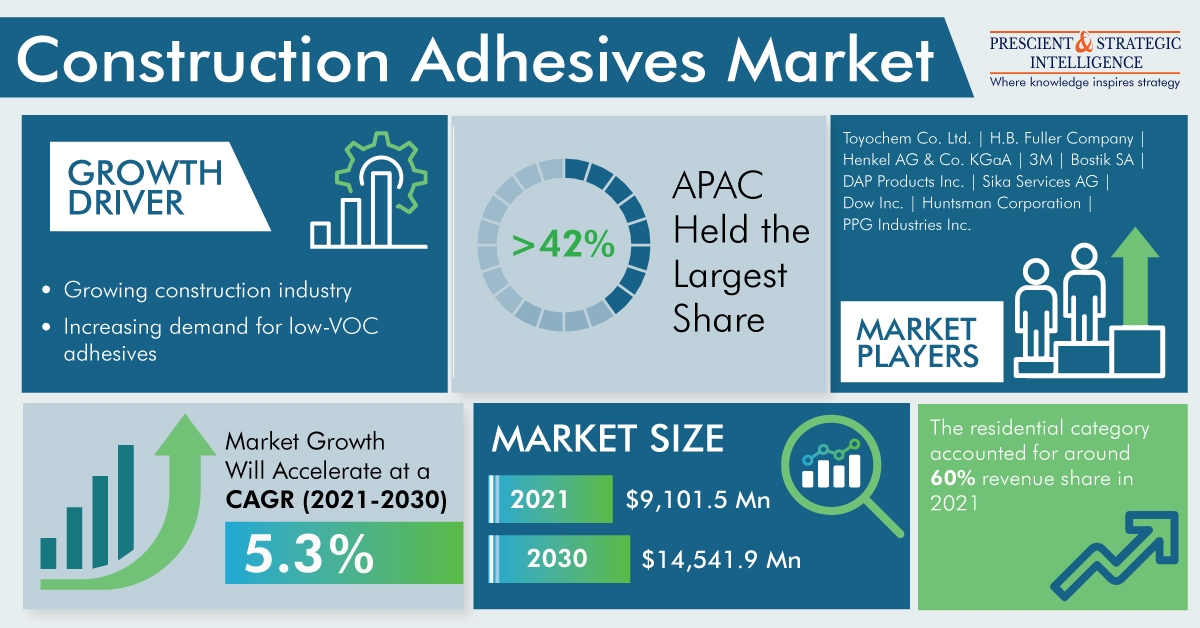

The size of the construction adhesives market was USD 9,101.5 million in 2021, and the figure is set to rise at a CAGR of 5.3% in the duration of 2021–2030, and to reach USD 14,541.9 million by the end of this decade, as per P&S Intelligence.

This can be credited to the rising construction sector, and snowballing demand for low-VOC adhesives, including water-based adhesives and pressure-sensitive adhesives.In 2021, the acrylic category held the largest revenue share of approximately USD 3,862.3, and this number will surge at a CAGR of 5.7% by the end of this decade. This can be ascribed to the fast development of the construction sector in the MEA and APAC regions. Acrylic adhesives are favorite in the construction industry mainly because of their solid bonding with substrates, outstanding water resistance, and better impact strength.

For example, China presently has a large number of airport building projects in the stage of expansion, including, Chengdu Shuangliu International Airport, Guangzhou Baiyun International Airport, and Beijing Capital International Airport. Furthermore, the Chinese government has publicized key strategies for the relocation of 250 million public to new megacities in the coming ten years.

In 2021, the residential category held the largest revenue share, of approximately 60%, credited to the high-volume utilization of construction adhesives in residential constructions.This can be ascribed to the increasing expenditure in residential construction actions than for commercial and industrial construction. According to an Indian government organization, the ‘Housing for All” scheme is purpose to fetch investments of USD 1.3 trillion in the residential industry by 2025.

In 2021, the APAC construction adhesives market held the largest market share of approximately 45%. This growth can be credited to the growing per-capita income, solid economic development, and increasing construction activity.Furthermore, the growing government investment in infrastructure and growing demand for low-VOC adhesives boost the growth of the market. For example, China is tended to invest approximately USD 13 trillion in the construction industry by 2030.