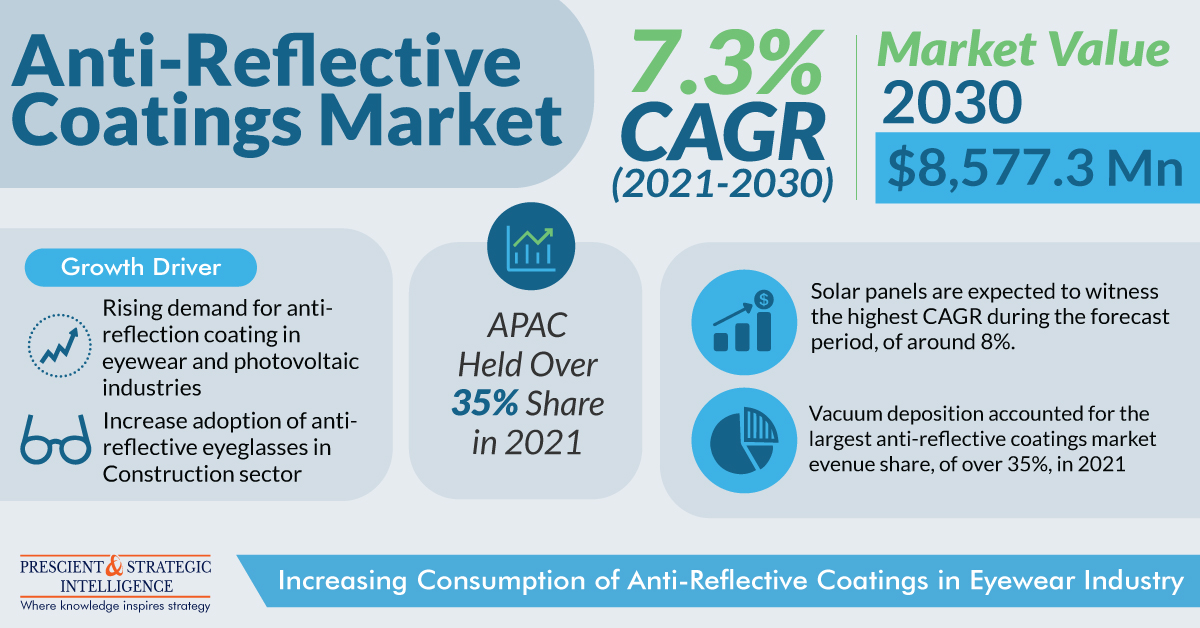

According to a statement by P&S Intelligence, the anti-reflective coatings market will generate USD 8,577.3 million, growing at a rate of 7.3%, by 2030.

The main factors boosting the growth of the industry include the increasing requirement for anti-reflection coats in the photovoltaic and eyewear industries, along with the rising implementation of anti-reflective eyeglasses in the construction sector.

Based on application, solar panels will witness the highest growth rate, of approximately 8%, in the years to come. This is credited to the growing requirement for low-cost solar cells with enhanced reliability and robustness, extensive adoption of these coatings in solar panels to rise their overall effectiveness, and the growing need to lessen photovoltaic surface reflection.

The growth of the anti-reflective coatings market is also driven by the increasing usage of these coatings in the eyewear industry, as the industry adopted such materials in high-light-transmitting products, for instance, eyeglasses and lenses.

Additionally, the advancement of technology in eyewear and the expansion of this industry because of the increasing prevalence of vision impairment, as well as the rising elderly populace, will further boost the growth of the industry.

In the past few years, vacuum deposition held the largest revenue share, of more than 35%, and it will propel with a significant growth rate throughout this decade. This is because of the extensive adoption of the deposition method in the application of antireflective coatings, because of its maximum adaptability, fast setting, affordability, and lesser environmental impact.

Moreover, North America accounted for a significant share of the anti-reflective coatings industry. This is credited to the existence of a large number of reputable companies, rising discretionary expenditure by consumers, growing consciousness about the benefits of coated eyeglasses, booming automotive sector, and increasing construction industry.

Key players have been involved in collaborations, acquisitions, partnerships, product launches, and investments to maintain a strong position in the industry.

Hence, the growing implementation of anti-reflective eyeglasses in the construction sector and the increasing demand for anti-reflection coatings in photovoltaic and eyewear industries will continue to drive the growth of the anti-reflective coatings industry in the years to come.