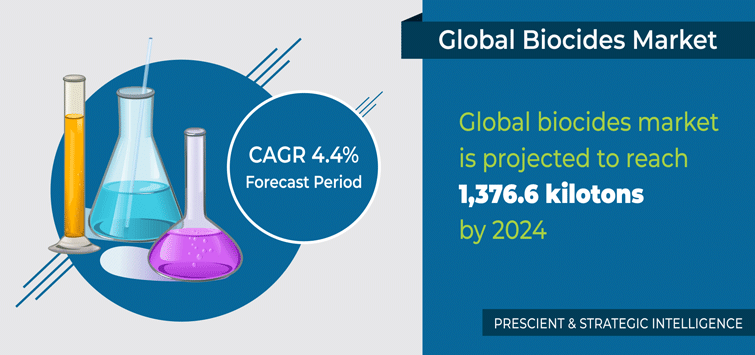

The biocides market is projected to rise in the near future, driven by the growing requirement for water treatment and the surge in the usage of biocidal products such as petrochemicals, homecare products, personal care, paintings, and coatings.

Biocidal products can be defined as the active substances for destroying, rendering harmless, deterring, or forces a controlling effect on harmful organisms by chemical or biological mediums. These products act as preservatives disinfectants, or pesticides, depending on their characteristics.

The halogenates are projected to generate the highest sales revenue in the biocides market, ascribed to the burgeoning requirement for water treatment. In addition, under the application segment, water treatment captures the largest share of the biocide’s industrial revenue, ascribed to the high demand for water treatment and potable water for both residential and industrial applications. It is projected to showcase significant sales in the coming years.

Moreover, APAC is projected to generate extensive sales revenue to the biocides industry, ascribed to the growing demand for water treatment in China, India, and other Southeast Asian countries for residential and industrial applications. The rise in the manufacturing capacity of the APAC nations leads to the expansion of the halogenates industry.

Several regulations and laws are enacted worldwide to control the usage of biocidal products. The European Union has implemented the biocidal products regulation (BPR), similarly, the U.S. FDA has also implemented several laws and regulations to monitor the application of the biocidal product, along with their active substances. It has resulted in a rise in the supervision level, and a ban on several biocidal products caused of their carcinogenic or mutagenic nature.

The growing demand for biocides for the preservation of varying types of consumer products, such as healthcare products, homecare, and water treatment for both residential and industrial purposes boost the market. Besides water treatment, biocidal products are widely used for equipment disinfection in the production, transportation, and storage of water.

Biocides are capable of preventing the growth of harmful organisms, such as protozoa, and bacteria as they act as antifouling or disinfectant agents. The major application of the biocides is at waterworks for maintaining microbiological quality before and during the distribution of water. It involves ensuring the acceptable microorganisms count level in the water and killing the rest pathogenic microorganisms.

The macro-economic progress of several countries and the rise in the disposable income of the people drive the demand for biocides. These products are highly used as preservatives, disinfectants, and sterilant in consumer products for alleviating microbial growth, resulting in bolstering demand for consumer products and resulting in extensive sales. In addition, the worldwide rise in the population fuels the demand for consumer products, resulting in the massive consumption of biocides.