The International Agency for Research on Cancer (IARC) states that 10 million cancer deaths and 19.3 million new cancer cases were recorded in 2020. As per the IARC, 1 in 5 people around the world develops cancer during their lifetime. Further, the World Health Organization (WHO) estimates that approximately 17.9 million human lives were lost due to cardiovascular diseases (CVDs) in 2019. Additionally, the WHO states that over 3 million people each year die of chronic obstructive pulmonary disease (COPD), accounting for over 6% of the global deaths.

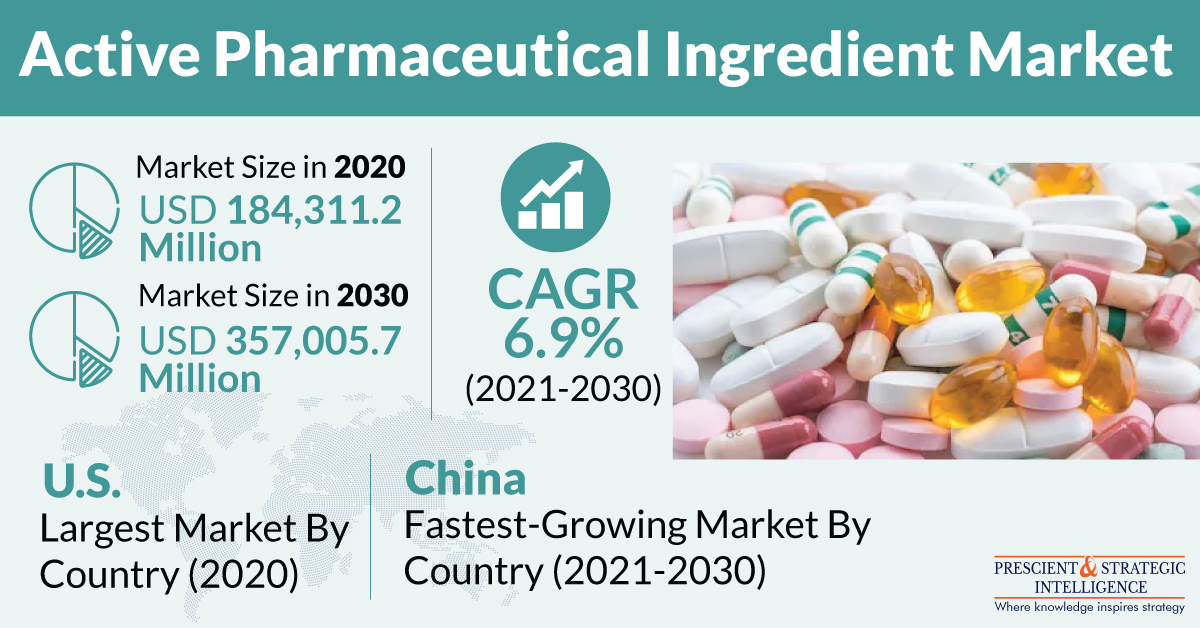

The rising incidence of such chronic diseases is projected to propel the active pharmaceutical ingredient (API) market at a CAGR of 6.9% during the forecast period (2021–2030). Additionally, P&S Intelligence states that the booming geriatric population will help the market revenue surge from $184,311.2 million in 2020 to $357,005.7 million by 2030. According to the United Nations Department of Economic and Social Affairs (UNDESA), the number of people aged 65 years or above will increase from 727 million in 2020 to around 1.5 billion by 2050.

Nowadays, captive and merchant manufacturers are producing generic and innovative APIs, which are available through online and offline channels. In contemporary times, innovative APIs are being used in higher quantities due to the mounting focus of pharmaceutical companies on developing new and more-effective medicines. In the coming years, captive manufacturers will emerge as the larger producer of APIs due to the stringent quality control and drug safety guidelines the pharma sector is subject to and the higher budgets captive companies possess for research and development (R&D).

The therapeutic application segment of the active pharmaceutical ingredient market is categorized into CVDs, communicable diseases, diabetes, oncology, pain management, respiratory diseases, and others. Among these, the oncology category held the largest market share in 2020, primarily on account of the high burden of cancer and extensive demand for highly potent APIs (HPAPIs) for cancer treatment. The WHO estimates that cancer caused approximately 10 million fatalities around the world in 2020. It also states that 1.93 million, 2.21 million, and 2.26 million people were diagnosed with colon and rectum, lung, and breast cancer, respectively, in 2020.

In recent years, pharma firms, such as Eli Lilly and Company, Mallinckrodt plc, Merck & Co. Inc., Lupin Limited, Johnson & Johnson, STADA Arzneimittel AG, AbbVie Inc., MSN Laboratories Pvt. Ltd., Novartis AG, Sun Pharmaceutical Industries Ltd., Pfizer Inc., AstraZeneca plc, and Sanofi, have been introducing new products, entering into collaborations and partnerships, and expanding their production capacities, to offer APIs to a greater number of customers. For example, in July 2021, Pfizer Inc. collaborated with Arvinas Inc. to develop and sell PROTAC estrogen receptor protein degrader ARV-471.

Globally, the North American active pharmaceutical ingredient market is expected to generate the highest revenue during the forecast period, owing to the rising burden of chronic diseases, mounting demand for specialty drugs and biologics, surging government focus on generic drugs, increasing technological advancements, and soaring number of R&D initiatives in the pharmaceutical industry. Moreover, the growing public awareness regarding numerous lifestyle-related diseases, such as diabetes, is expected to drive the API demand in the region.